Car Insurance After an Accident: What to Know

How much does car insurance go up after an accident?

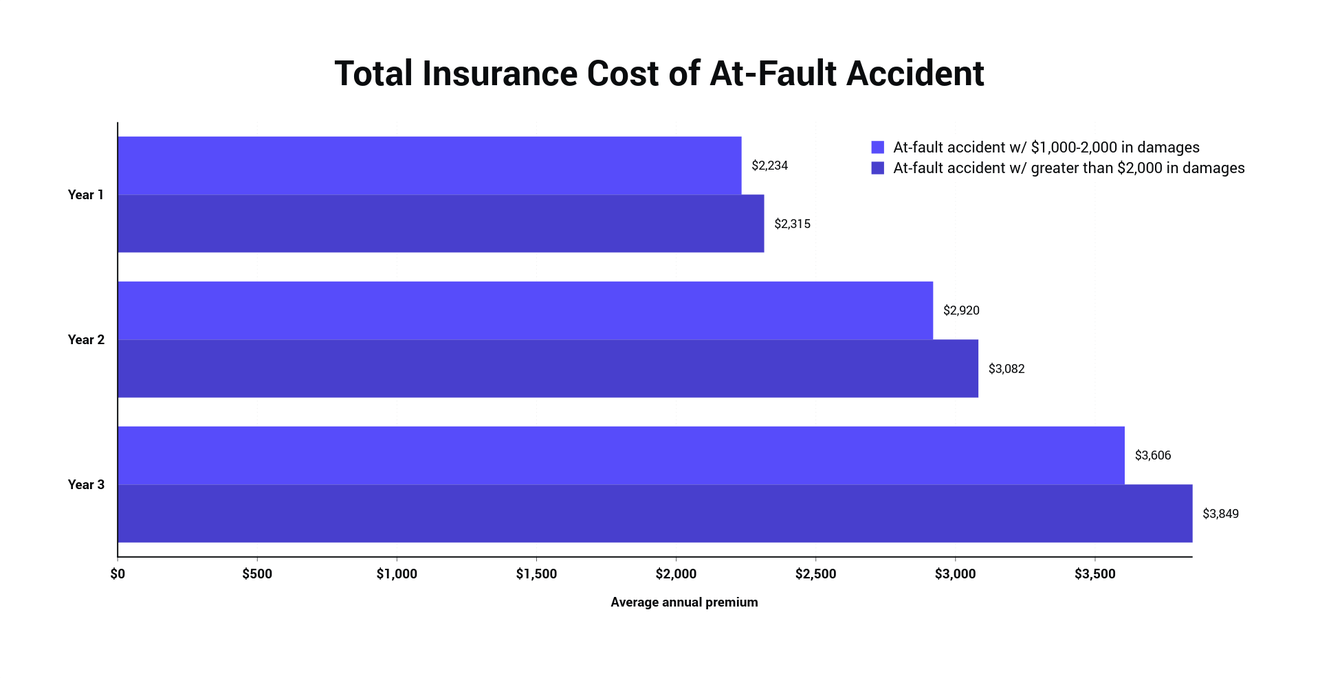

After an at-fault accident, policyholders can expect insurance rates to rise by $767 per year — that's an increase of almost 50% from the average rate without an accident ($1,548). Most accidents, tickets and moving violations stay on a driver's record for as long as three to five years. Over a three-year period, that could add up to $2,300 in extra insurance premiums.

Read on to learn more about how to handle car insurance after an accident. Or, check out personalized car insurance quotes to ensure you're not getting overcharged for auto insurance.

Which insurance company is the best after an accident?

Of the major car insurance companies, the cheapest rates after an accident come from USAA, GEICO, and State Farm. Both GEICO and USAA advertise "accident forgiveness" options that can minimize the increase of your premiums, though these must be purchased separately as an add-on and must be in place at the time of the accident. Bear in mind that these options may not be available in every state.

While you can definitely expect higher rates after an auto accident, each insurer will weigh them differently. To illustrate the financial ramifications of a collision, we gathered car insurance rates from some of the most popular auto insurance companies in the U.S. (methodology). See below how much a collision could cost, depending on the insurer you choose. Keep in mind that insurers will typically charge you higher premiums over a three-year period after an at-fault accident.

| Company | Avg. Monthly Premium | Avg. Annual Premium |

|---|---|---|

| USAA | $161 | $1,927 |

| State Farm | $167 | $2,005 |

| Nationwide | $194 | $2,334 |

| GEICO | $195 | $2,344 |

| Farmers | $209 | $2,508 |

| Progressive | $245 | $2,936 |

| Allstate | $290 | $3,482 |

The Zebra’s Dynamic Insurance Rating Tool data methodology

The Zebra’s Dynamic Insurance Rating Tool for home and auto insurance rates utilizes the latest ZIP code-level rate filings from across the U.S., sourced from Quadrant Information Services and S&P Global. These filings, typically updated annually or biennially by insurers, are verified through Quadrant’s QA process and then integrated into The Zebra’s estimator.

The displayed rates are based on a dynamic home and auto profile designed to reflect the content of the page. This profile is tailored to match specific factors such as age, location, and coverage level, which are adjusted based on the page content to show how these variables can impact premiums.

For a comprehensive understanding, see our detailed methodology.

Allstate is typically the most expensive car insurance company after an at-fault accident, while USAA is the cheapest. While the table above outlines the average rates for drivers after an at-fault accident, the table below shows national averages in general (without an at-fault accident in recent history).

| Company | Avg. Monthly Premium | Avg. Annual Premium |

|---|---|---|

| USAA | $106 | $1,277 |

| State Farm | $117 | $1,405 |

| GEICO | $142 | $1,698 |

| Progressive | $147 | $1,762 |

| Nationwide | $149 | $1,787 |

| Farmers | $177 | $2,129 |

| Allstate | $211 | $2,536 |

| Liberty Mutual | $215 | $2,576 |

Compare rates and find an affordable insurance policy.

Why do car insurance rates go up after an accident?

Auto insurance rates commonly increase after an accident for one of a few reasons:

Surcharges triggered by an at-fault accident include the cost of the claim adjuster's time, fees related to the claims representatives, and the cost of parts and labor. These fees usually aren’t accounted for in your monthly premium, and thus increase if you utilize them. It helps to know when to forgo making a claim and settling out-of-pocket, especially if it's a minor accident. You may be able to discuss the percentage increase with a representative from your insurance company to help with your decision.

Historical data show drivers who have been in a crash are more likely to get into another accident. These drivers present more risk — and potentially more expense — to insurance companies than do clients with clean records. An insurance company accounts for this added risk by increasing the cost of a car insurance policy for a "high-risk driver" involved in a collision.

When do insurance rates go down after an accident?

While the timing may vary based on location and the circumstances surrounding the incident, most insurance companies will drop rates three to five years after the incident (assuming you've kept a clean driving record during that time). If the collision occurs long before your policy renewal date, this penalty period can stretch beyond the typical three-to-five-year window.

If the penalty period for an accident is set to expire in January but your policy ends in June, the accident will not be removed from your insurance bill until your policy renews — or you specifically ask. If you have an accident on your insurance record, keep track of the date and chargeable time. Your insurance company will not do this for you. This can help you avoid a longer-than-necessary surcharge period.

Three years is a common penalty period following a claim for property damage or collision. Depending on your state and your insurance company, policyholders may be penalized for a longer period of time following these more severe violations:

- DUI/DWI

- Bodily injury claim

- Reckless driving

- Multiple — or excessive — violations within a certain time

- An accident resulting in serious bodily harm or death

After the accident falls off your driving record, consider adding accident forgiveness to your auto insurance policy to avoid a surcharge should you be involved in another accident. Most insurance companies require a driver to be claim- or accident-free for a period of time (typically three to five years) to receive accident forgiveness.

How to find cheap car insurance after an accident

The amount by which car insurance premiums go up after an accident depends on many variables. The specifics of the accident, your vehicle, you, and most importantly, your insurance company.

While it's definitely not recommended for newer or higher-priced vehicles, foregoing extra coverage options such as comprehensive or collision coverage can dramatically lessen your monthly rates. Liability coverage is often enough to keep you legal, but your own vehicle would have no coverage.

If you’re being charged a significant amount in additional premiums after an accident, it helps to shop around for a better rate. Every auto insurance company uses its own rating methods to calculate premiums, so you might be able to find cheap car insurance after an accident if you compare rates thoroughly.

Frequently asked questions

Shop for rates online and start saving.

Related Content

RECENT QUESTIONS

Other people are also asking...

Can I add coverage after I've had an accident?

Is a hydroplaning accident my daughter's fault?

What can I do if someone hit my car and left a note but they won't answer or return my calls?

At-fault driver gave me the wrong information

About The Zebra

The Zebra is not an insurance company. We publish data-backed, expert-reviewed resources to help consumers make more informed insurance decisions.

- The Zebra’s insurance content is written and reviewed for accuracy by licensed insurance agents.

- The Zebra’s insurance editorial content is not subject to review or alteration by insurance companies or partners.

- The Zebra’s editorial team operates independently of the company’s partnerships and commercialization interests, publishing unbiased information for consumer benefit.

- The auto insurance rates published on The Zebra’s pages are based on a comprehensive analysis of car insurance pricing data, evaluating more than 83 million insurance rates from across the United States.