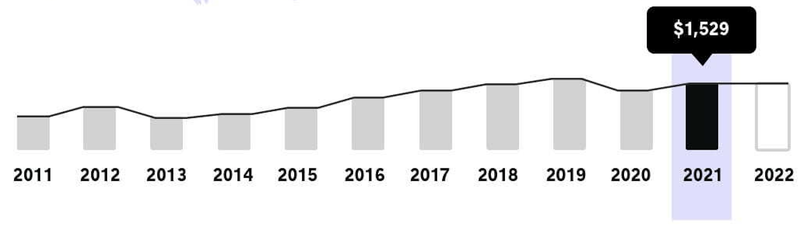

Individual results may vary, but for many 2021 was not the best year. Year 2 of the COVID-19 pandemic came equipped with political turmoil, historic weather events and…rising insurance rates.

Insurance getting more expensive is generally something we can rely on right alongside death and taxes, but in 2020 things changed. For the first time since 2013, rates actually went down.

The reasons for that were directly connected to the COVID pandemic. People were driving less and filing fewer claims, so rates were lower.

However, in 2021 things started to return to normal. And so car insurance rates rose 3% from 2020 to 2021 and will likely continue to rise in 2022.