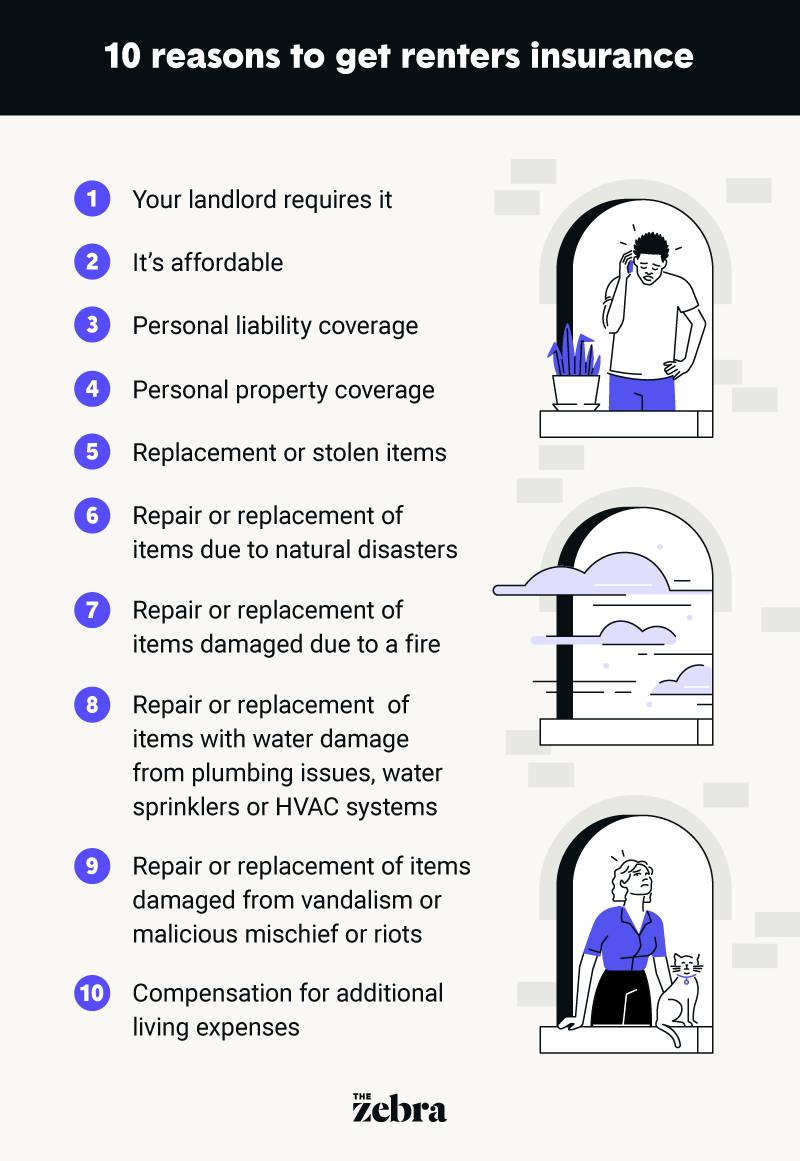

While no one enjoys imagining worst case scenarios, preparation for such a situation can elevate some stress later should one arise. Could you afford to replace your laptop, television, clothes and furniture if your apartment suddenly caught fire? What about adding a hotel stay into the mix while your apartment is rebuilt?

Many renters aren’t sure whether they should opt for renters insurance. However, there are more than a few reasons to get renters insurance, and most favor you over your landlord. In fact, if your apartment were to catch fire, you would receive compensation for your damaged belongings.

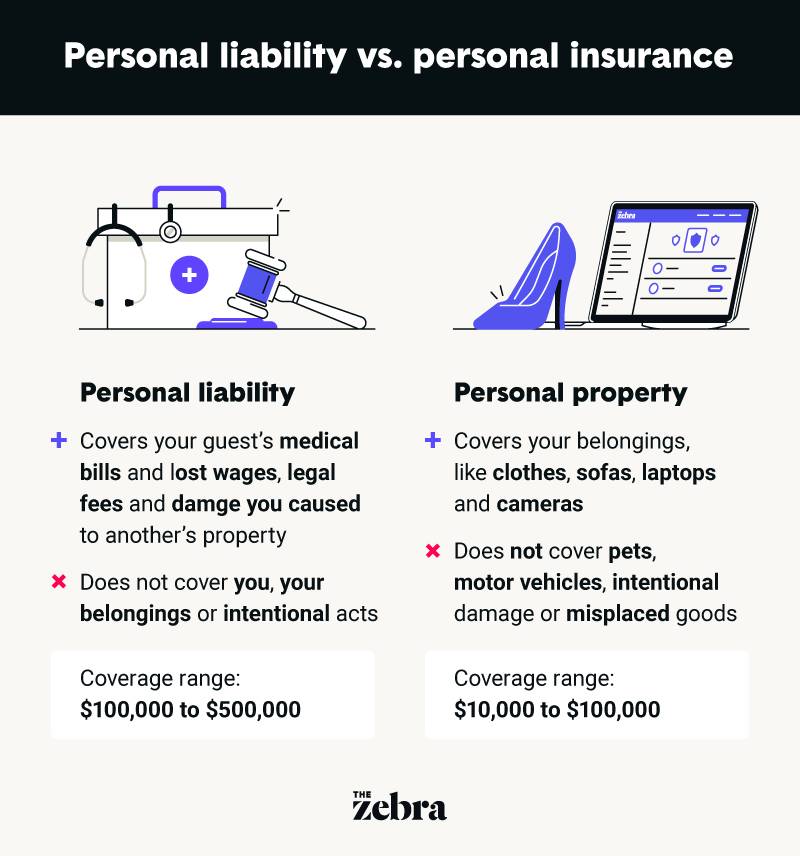

Are you now wondering, “Do I need renters insurance?” If you’re curious about what renters insurance covers, keep reading to learn about the different coverage options and scenarios where you’ll have protection.