The early 2020s have facilitated homebuying at a large scale, with mortgage interest rates sitting near record-low levels for extended periods of time.

Since Freddie Mac began tabulating annual average interest rates for 30-year fixed-rate mortgages (FRM) in 1971, interest rates have never been this low. As of this writing, a 30-year FRM is at 3.25%. For context, the all-time high was 18.63% in 1981.

In addition to opening homebuying up to a greater number of people, low interest rates have homeowners asking whether now is the right time to refinance their homes. While there are certainly attractive reasons to do so, refinancing your home loan should be considered carefully. Here’s how to know when it’s right for you.

How home refinancing works

Refinancing a mortgage means you’re taking out a new loan to pay off your original loan. We’ll examine why you might want to do that below. The refinance process isn’t much different from getting your first mortgage loan.

You’ll shop around and compare mortgage rates, fees, terms and other factors with mortgage lenders to see which has the best offer. Your current mortgage lender may reach out to you, as well, especially if the company finds an offer that compares favorably with your current loan.

Why refinance your home?

There are a number of reasons to refinance. Many homeowners refinance to change their mortgage loan term or rate type, to cash out significant equity in their home or to lower their interest rate and payment.

Interest rates exist as a way for lenders to get compensated for the inability to use the money they’re loaning. Think of interest as a rental or leasing charge to use your home until the mortgage is paid off in full. The interest rate is applied to the principal—if the borrower appears to be higher risk, a lender will charge a higher rate.

While the nation has an average interest rate, your personal rates may be higher or lower. Some of the factors that determine your interest rate include your credit score, home location, price, down payment, interest rate type, loan amount and loan type. For example, a higher credit score, larger (at least 20 percent) down payment, and a shorter term each typically results in a lower interest rate.

Types of home refinancing

There are three main types of home refinance loans:

- In a rate and term refinance loan, the homeowner seeks to change the interest rate and/or loan term without changing the total amount of the loan.

- In a cash-out refinance loan, the homeowner cashes out a portion of the home’s equity. This gives them a quick amount of cash-on-hand, but also likely will create a higher monthly payment and interest rate.

- In a cash-in refinance loan, the homeowner pays money to reduce their new mortgage balance. This is a less common type of loan, but can help with removing private mortgage insurance or keeping your mortgage rate below a certain threshold.

Before you jump into refinancing to find a lower interest rate, take the time to research the pros and cons.

Pros of home refinancing

Refinancing your home can lower your monthly payments over the course of your mortgage. This can occur via adjusting the interest rate, the length of your loan or both.

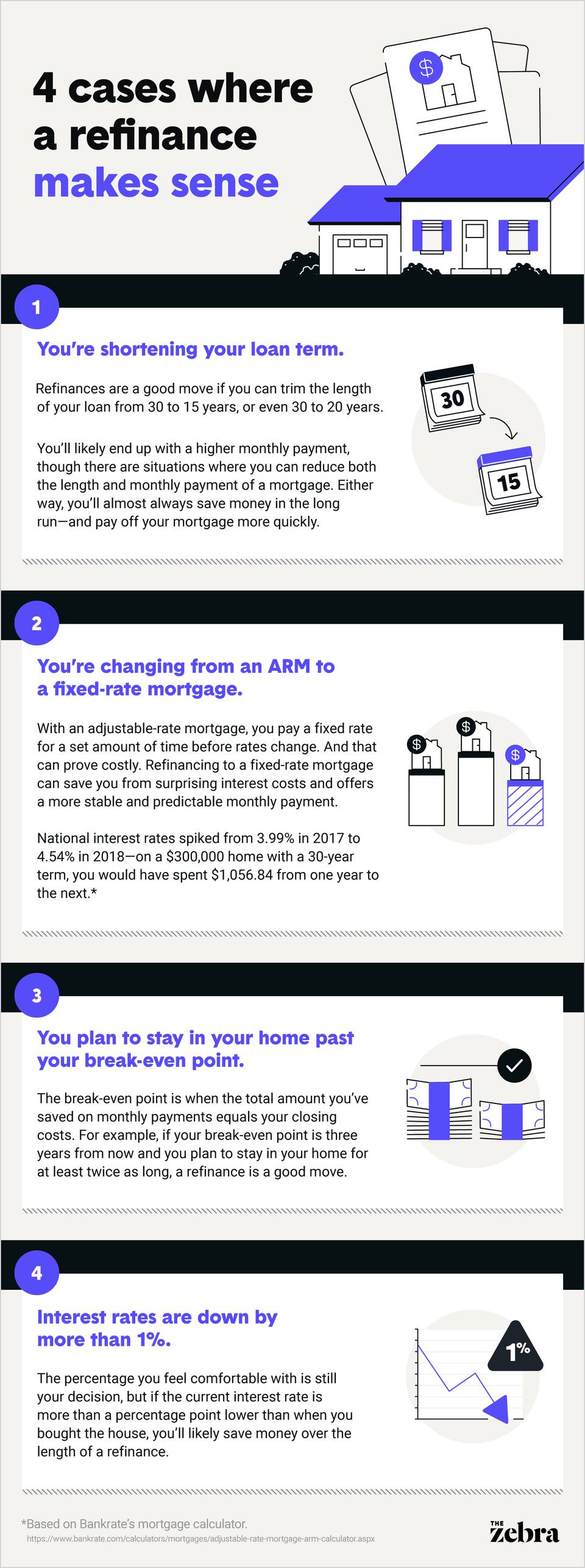

Using a home refinance calculator helps you determine your monthly payments and also identifies your break-even point. This is the amount when the savings from your monthly payments equal your closing costs. For example, if refinancing your mortgage lowers your monthly payments by $100 and has closing costs of $3,600, your break-even point is 36 months (or three years). If you’re planning to stay in your home for a long time past the break-even point, a mortgage refinance can help you save money over time.

Mortgage refinancing is also a great way to change the terms of your home loan. If you signed up for a 30-year fixed-rate mortgage (FRM), for instance, you may qualify for a 20-year or 15-year FRM when refinancing. Lowering the term can lead to saving tens of thousands of dollars in interest over the life of the loan, and result in you owning your home mortgage-free more quickly. Similarly, you can move from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage, leading to predictability and stability, plus potential cost savings.

In a cash-out refinance, you’ll also receive a lump sum of cash when you refinance. This can be helpful in paying for costly events, such as buying a car, going through a divorce or starting a business. However, this type of refinance increases the total amount of the loan, which can cost you in the long run. You could also reduce your home equity.

Cons of home refinancing

While cost is one of the largest pros of refinancing, it can also be a major con. You may be able to lower your monthly mortgage payment, but you still have to consider interest rates and closing costs. Even though you’ve already purchased your home, these costs still exist when you refinance, and will usually be anywhere from three to seven percent of your mortgage. However, those vary from lender to lender and may include additional fees, so make sure you’re seeing all costs before you commit. That includes any prepayment penalties from paying off your existing mortgage. Some loans will charge you extra if you pay off the loan too quickly.

A refinance can also add extra years and money to your mortgage through amortization, or the process of paying off debt in regular increments of interest and principal so you can fully repay the loan by the maturity date. Home and auto mortgages with fixed monthly payments charge more interest early on. As the overall total amount of the loan decreases, the portion of your monthly payment that’s going toward the principal amount increases. Refinancing puts that amortization back in action.

Let’s say your current mortgage is a 30-year, fixed-rate mortgage, and you’re five years into the mortgage. If you refinance to another 30-year, fixed-rate mortgage, it’s like you’re starting all over again. You’ll now spend 35 years paying the home off, instead of 30. And depending on the interest rates, you may even spend more money than if you had just kept your original loan.

Finally, you also have to apply and qualify for a refinance. If you’re struggling with your current mortgage, it can be difficult to get a new loan. A lender needs to run income and credit checks, which adds a hard inquiry to your credit report, reducing your credit score by a few points. If you shop around for a mortgage over the span of multiple months, your credit score could drop from several inquiries.

Depending on the circumstances, a refinance can be a great decision or end up doing more harm than good.

Thinking about refinancing your home mortgage? Here are four occasions when it might make sense: